Introduction

FRP pressure vessels have moved from a specialty industrial product to the preferred material choice across water treatment, chemical processing, and oil and gas. That shift is now showing up in market data — and it carries real implications for facility operators managing aging FRP assets across North America.

Fiber-reinforced plastic pressure vessels offer distinct advantages over steel alternatives:

- Resist corrosion in chemically aggressive environments where metal degrades rapidly

- Weigh significantly less, reducing installation and structural support costs

- Require less ongoing maintenance over their service life

- In certain environments, surpass stainless steel for corrosive liquid containment

AFTR's field experience across chemical plants and water treatment facilities confirms this performance gap is widening as resin and laminate technology improves.

This article covers where the global FRP pressure vessel market stands today, what's driving growth, which industries and regions are leading demand, and what a growing installed base means practically for facility operators managing these assets.

Key Takeaways

- The broader FRP vessels market is valued at approximately $4.45B in 2026, projected to reach $6.55B by 2031 at an ~8% CAGR

- FRP is growing nearly twice as fast as the all-material pressure vessel market (~4-5% CAGR)

- Water and wastewater treatment accounts for roughly 35% of demand, making it the single largest application segment

- Asia-Pacific leads with nearly 45% market share; North America ranks second

- FRP vessels typically carry a 20–30 year service life, meaning a large share of the installed base is now entering peak maintenance and relining cycles

FRP Pressure Vessel Market Size: Where Things Stand Today

Current Valuations and Growth Rates

Two major analyst datasets bracket the market's current size. Mordor Intelligence's FRP vessels market report places the broader FRP vessels market at $4.45 billion in 2026, forecast to reach $6.55 billion by 2031 at an 8.03% CAGR. An earlier MarketsandMarkets dataset estimated the market at $3.9 billion in 2022, projecting growth to $5.7 billion by 2027 at an 8.0% CAGR.

Both reports use a broader FRP vessels category that includes non-pressure storage vessels alongside true pressure vessels. No standalone global figure exists for pressure vessels alone, but both datasets agree: multi-billion dollar growth through the early 2030s is the baseline expectation.

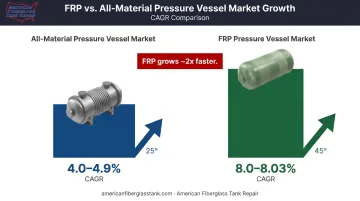

How FRP Compares to the Broader Pressure Vessel Market

The overall pressure vessel market — covering steel, alloy, and composite vessels — is projected at a 4.0–4.9% CAGR through 2030-2031. FRP is growing at roughly double that rate, which points to a real change in material preference, not just general market expansion.

As demand for corrosion-resistant containment grows, FRP is capturing share from metal alternatives across end-uses — a trend that shows up clearly in how the pressure rating segments are performing.

Pressure Ratings Across the Market

The FRP pressure vessel market spans a wide performance range:

- Medium pressure (10–250 bar): Holds 46% market share as of 2025, making it the largest segment by volume

- High pressure (≥250 bar): Growing at 8.92% CAGR — the fastest-growing pressure class

- Commercial products: Pentair Codeline vessels are available at 150, 300, 450, 600, 1,000, and 1,200 psi operating pressures

AFTR has observed demand across this full range — from low-pressure chemical storage tanks to higher-pressure RO membrane housings used in water treatment systems.

Key Drivers Fueling FRP Pressure Vessel Market Growth

Water Infrastructure Investment

The water and wastewater sector is the single largest demand driver for FRP pressure vessels. The scale of unmet need is substantial: UN data shows roughly 42% of household wastewater was not safely treated before discharge in 2022.

The World Bank estimates developing countries spend approximately $164.6 billion per year on the water sector — against an annual shortfall of $131–141 billion for universal safe water and sanitation.

That gap means sustained infrastructure buildout — and FRP pressure vessels are central to it, housing RO membranes, sand filters, and multi-media filtration systems that require corrosion resistance above all else.

Corrosion Resistance in Aggressive Chemical Service

Facilities handling acids, alkalis, and oxidizing agents switch to FRP because metal vessels fail prematurely in those environments. AFTR's field teams encounter this regularly across chemical plants, water treatment facilities, and wastewater operations. The most common chemical services include:

- Sodium hypochlorite (NaOCl) — highly oxidizing, rapidly degrades metal

- Sodium hydroxide (NaOH) — caustic, attacks carbon steel

- Ferric chloride (FeCl3) — corrosive flocculant used in wastewater treatment

- Hydrochloric acid (HCl) — extremely aggressive toward most metals

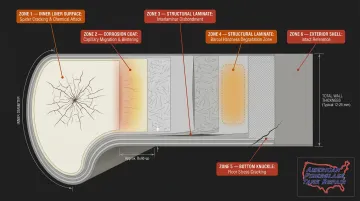

When these vessels degrade, AFTR inspectors most commonly document spidering, disbondment, Barcol hardness loss, floor stress cracking, and capillary migration of product beneath the corrosion coat. That last failure mode is the most dangerous — it's invisible without proper NDE testing.

Regulatory Compliance and Environmental Standards

Two regulatory frameworks routinely push operators toward FRP over metal:

- EPA hazardous-waste tank rules — require demonstrated chemical compatibility between stored materials and tank construction

- NSF/ANSI 61 — governs materials in direct contact with drinking water, where metal corrosion risks contaminant leaching

In corrosive service applications, FRP satisfies both frameworks where metal often cannot.

Technology and Manufacturing Advances

Improvements in filament winding technology and resin systems have expanded FRP's operating envelope. NOV's Fiber Glass Systems facility achieved ASME BPVC.X certification, enabling achievable design pressure to increase from 145 psi to 290 psi for glass-reinforced epoxy components. Vinylester and epoxy resin systems now allow FRP vessels to handle higher temperatures and more aggressive chemistries than older isophthalic polyester systems — bringing high-temperature acid service and concentrated caustic storage within FRP's viable range.

Industry Segments Driving FRP Pressure Vessel Demand

Water and Wastewater Treatment

Water and wastewater treatment accounts for approximately 35% of total FRP vessel demand , the largest single application segment. FRP vessels serve as membrane housings for RO systems, sand filter vessels, and multi-media filtration housings where continuous exposure to chlorinated water and treatment chemicals would corrode metal alternatives within years.

AFTR's wastewater work covers municipal treatment plants, industrial effluent systems, and potable water storage, including tank relining after sodium hypochlorite degradation and ferric chloride storage vessel restoration.

Chemical Processing and Storage

Chemical plants rely on FRP pressure vessels for storing and processing corrosive acids, alkalis, and solvents. U.S. chemical-industry capital spending reached $34 billion in 2024 (up 4.1% year-over-year) and is projected to grow at 2.9% annually through 2028. That expansion directly drives demand for corrosion-resistant containment.

For chemical service environments, AFTR selects custom-blended resins (isophthalic polyester, terephthalic polyester, vinylester, or epoxy) matched to each specific chemistry and operating temperature.

Oil and Gas

FRP vessels serve produced water handling, injection systems, and offshore platform applications where weight reduction matters significantly. Offshore platforms favor FRP over steel for produced water systems, where saltwater exposure and weight constraints make corrosion-resistant composites the practical choice. Even as energy investment cycles, produced water volumes remain high enough to sustain steady demand for FRP containment.

Emerging Applications

Several sectors are accelerating FRP adoption:

- Pharmaceuticals: non-reactive containment for process fluids and CIP (clean-in-place) systems

- Food processing: FDA-compliant vessel materials for food-grade fluids, including heated FRP tanks that AFTR services through heating panel repair and relining

- Power generation: cooling water and chemical dosing systems where corrosion resistance is required

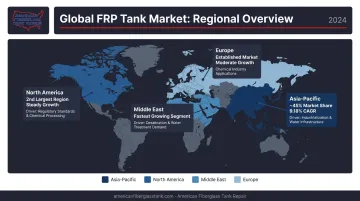

Regional Market Breakdown: Where Growth Is Concentrated

| Region | Market Share | Growth Rate | Key Drivers | |--------|-------------|-------------|-------------|\n| Asia-Pacific | ~45% (2025) | 9.18% CAGR | Industrialization, water infrastructure, petrochemicals | | North America | Second-largest | Steady growth | Water infrastructure upgrades, high regulatory standards | | Middle East | Growing | Significant | Desalination, petrochemical expansion | | Europe | Established | Moderate | Environmental regulation, chemical industry |

Asia-Pacific is both the dominant and fastest-growing region, with China as the largest country-level market and India as a significant emerging market. The Asian Development Bank estimates the region requires an estimated $4 trillion in water, sanitation, and hygiene investments through 2040 — investment that flows directly into FRP vessel demand.

North America benefits from strong industrial infrastructure, high regulatory standards that favor corrosion-resistant materials, and ongoing municipal water and wastewater system upgrades. Aging treatment facilities across the U.S. are a consistent driver — many plants are operating FRP vessels well beyond their original design life, creating sustained demand for both new installations and maintenance services.

Middle East demand is driven by desalination — Saudi Arabia alone had 30 SWCC desalination plants in operation with a 2023 approved budget of $6.6 billion for additional capacity. FRP pressure vessels are central to RO-based desalination as membrane housings.

Europe, while growing at a more moderate pace, maintains steady demand through environmental compliance requirements and a well-established chemical processing sector. Together, these four regions account for the bulk of global FRP pressure vessel consumption, with Asia-Pacific's growth trajectory widening its lead through the decade.

Challenges and Restraints in the FRP Pressure Vessel Market

Raw Material Price Sensitivity

FRP vessels depend on glass fiber, carbon fiber, and polymer resins. ACMA's 2024 State of the Industry Report notes that resin and fiber prices declined in 2023 due to economic softening, but flagged 2024 uncertainty from interest rates and supply-chain restructuring. Energy cost fluctuations pass through to resin prices, creating margin pressure for manufacturers and unpredictable procurement costs for buyers.

Competition from Alternative Materials

FRP doesn't automatically win every application. Competing vessel materials include:

- Lined steel — common in high-pressure systems where structural strength takes priority

- Duplex stainless steel — preferred for high-temperature service where metal's thermal performance is advantageous

- Thermoplastic-lined metal vessels — used in aggressive chemical environments requiring chemical resistance without full composite construction

Buyers making lifecycle cost decisions weigh all options. FRP's advantage is strongest in corrosive, moderate-temperature service conditions where its weight and chemical resistance outperform metal alternatives.

Inspection and Maintenance Expertise Gaps

A growing installed base of FRP pressure vessels requires a parallel supply of qualified inspectors — and that supply is lagging. FRP composite laminate is brittle under overload rather than ductile, and failure modes like delamination and capillary migration require specialized NDE techniques to detect. Visual inspection alone misses the most dangerous subsurface defects.

Companies like AFTR (American Fiberglass Tank Repair) respond to this gap with FTPI-certified inspectors, engineer-supervised field teams, and ultrasonic, laser, and high-intensity backlight testing methods. Bridging the expertise gap at the field level is as important to market health as any upstream manufacturing trend.

What FRP Market Growth Means for Vessel Owners and Operators

A growing FRP pressure vessel market means a growing installed base and a growing population of aging assets. Vessels installed in the late 1990s and early 2000s are now 20–25 years into service, reaching the stage where corrosion barrier degradation, capillary migration, laminate disbondment, and joint cracking become operational concerns rather than theoretical risks.

AFTR has seen demand for professional FRP repair and maintenance services increase fivefold over the past 25 years, driven directly by the accumulation of aging vessels across water treatment, chemical, and industrial facilities.

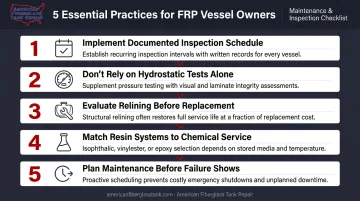

The most important actions for vessel owners operating aging FRP assets:

- Implement a documented inspection schedule. Periodic inspections using ultrasonic, laser, and backlight testing catch liner failures and capillary migration before they become containment events.

- Don't rely on hydrostatic tests alone. A vessel can pass a hydrostatic test and still have developing subsurface degradation that will cause failure.

- Evaluate relining before replacement. AFTR's field crews have restored vessels storing sodium hypochlorite, sodium hydroxide, ferric chloride, and HCl by fabricating new corrosion barriers in place, extending service life at a fraction of replacement cost.

- Match resin systems to chemical service. Relining with the wrong resin accelerates degradation rather than preventing it. AFTR specifies custom-blended isophthalic, terephthalic, vinylester, or epoxy systems based on stored chemical, concentration, and operating temperature.

- Plan maintenance before failure shows. Visible signs of degradation typically mean corrosion has already reached the structural body of the vessel.

The market's growth trajectory is useful context for capital planning. The more actionable priority is having a documented inspection and maintenance program in place, particularly as regulatory scrutiny on industrial containment assets tightens across North America. For facilities without a formal program, now is the right time to establish one.

Frequently Asked Questions

What is the current size of the global FRP pressure vessel market?

The broader FRP vessels market is valued at approximately $4.45 billion in 2026 and projected to reach $6.55 billion by 2031 at an 8% CAGR, based on Mordor Intelligence data. An earlier MarketsandMarkets estimate placed the market at $3.9 billion in 2022 growing to $5.7 billion by 2027.

What industries use FRP pressure vessels the most?

Water and wastewater treatment is the dominant application, representing roughly 35% of global demand. Chemical processing and oil and gas follow as significant segments. Pharmaceuticals and food processing are growing application areas as clean, non-reactive containment requirements expand in regulated industries.

Why are FRP pressure vessels preferred over steel or metal alternatives?

FRP's primary advantages are corrosion resistance in chemically aggressive service environments, significantly lighter weight, and lower lifecycle maintenance costs. In applications involving acids, alkalis, chlorinated water, and oxidizing chemicals, FRP consistently outperforms carbon steel and requires less intervention to maintain containment integrity.

Which region is leading FRP pressure vessel market growth?

Asia-Pacific leads with approximately 45% market share and a projected 9.18% CAGR, driven by rapid industrialization and massive water infrastructure investment in China, India, and Southeast Asia. North America and Europe are established markets with steady ongoing demand from industrial and municipal water infrastructure upgrades.

What are the main challenges facing the FRP pressure vessel market?

The three primary challenges are raw material price volatility for glass fiber and polymer resins, competition from lined steel and duplex stainless steel in high-pressure applications, and a growing shortage of qualified inspectors who can detect composite failure modes like delamination and capillary migration.

How long do FRP pressure vessels last, and what affects their lifespan?

FRP vessels can last 20–30+ years with proper maintenance — Pentair's 80K series membrane housing carries a design life of over 25 years. Lifespan shorteners include corrosion barrier degradation, deferred maintenance, improper resin specification, and UV exposure for outdoor installations. Proactive relining before the structural body is compromised can extend vessel life at a fraction of replacement cost.